Via Metal Miner

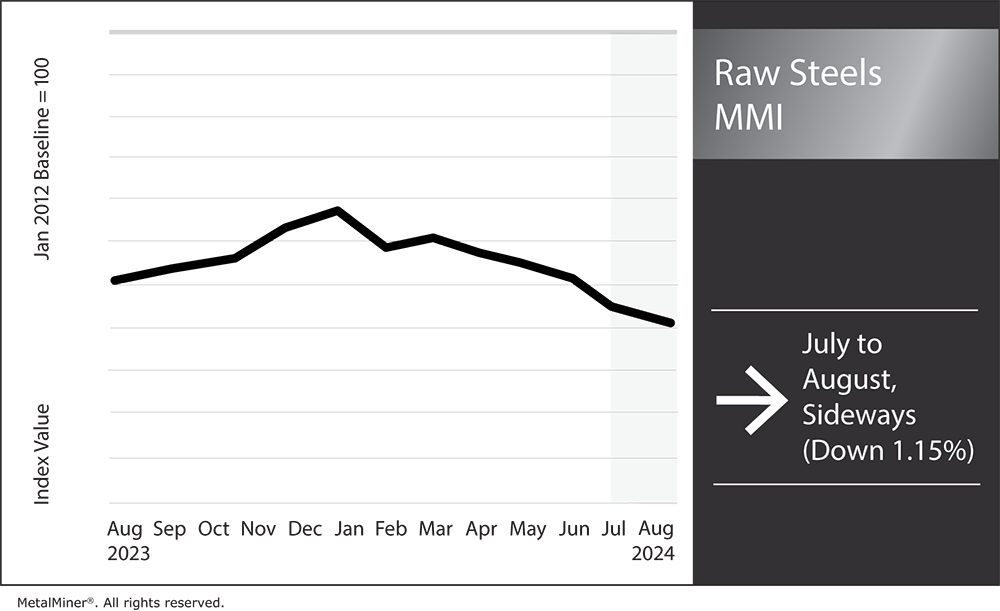

The Raw Steels Monthly Metals Index (MMI) moved sideways, with a 1.15% decline from July to August.

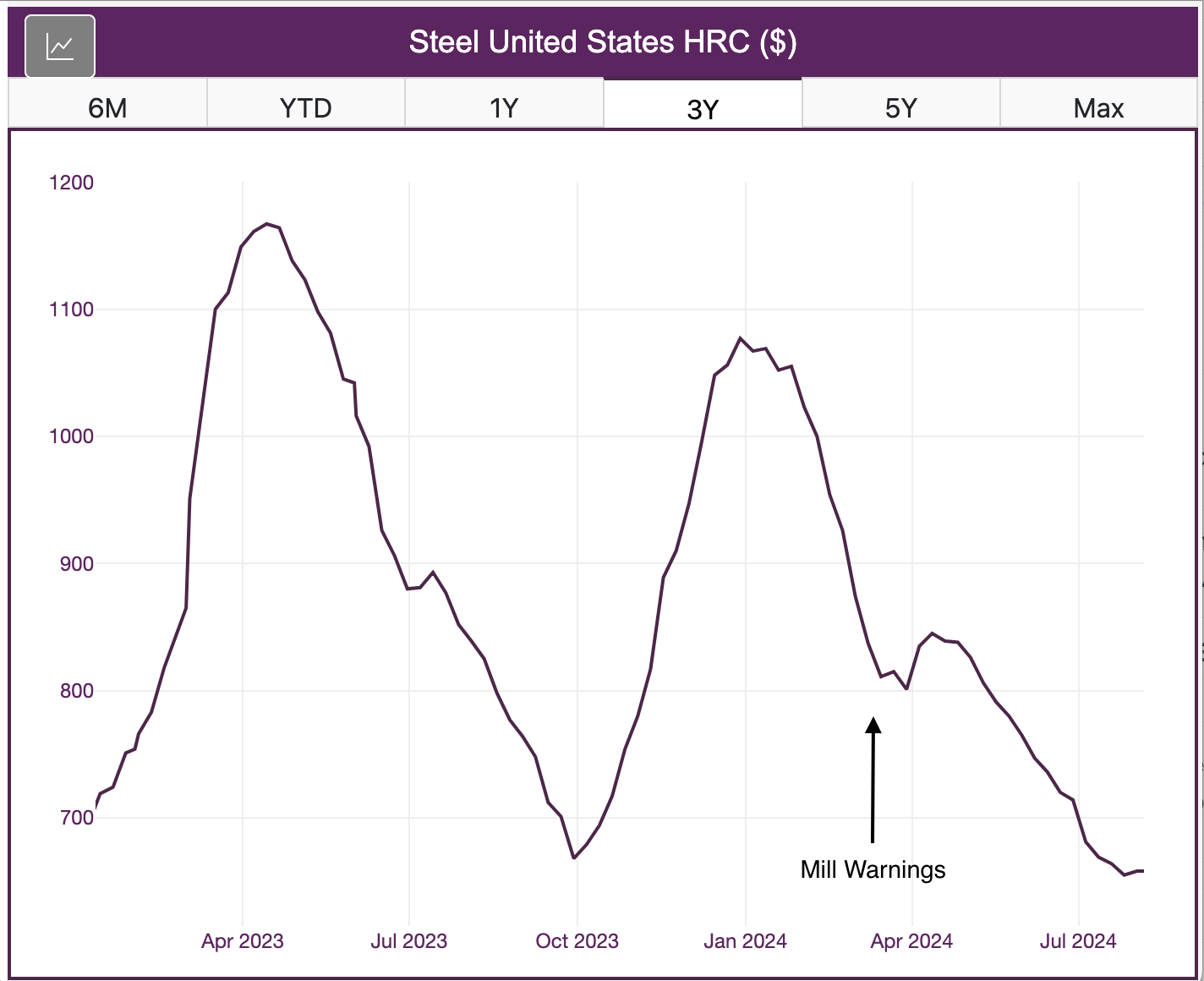

U.S. steel prices remained in search of a new bottom by the close of July. HRC prices dropped a total of 8.26% during the month, pushing them to their lowest level since December 2022. However, prices appeared to stabilize by the first week of August as mills attempted to invert the bear trend with the announcement of higher prices.

Rumors of a Bottom Echo April Warnings

Despite seemingly bearish market signals, rumors began to emerge in late July that U.S. steel prices were on the verge of a bottom. HRC prices have largely held within a steady downtrend since prices found a peak at the close of 2023, followed by a nearly 40% decline throughout 2024.

The lone exception to otherwise bearish steel prices occurred at the close of March. Ahead of planned maintenance, mills warned of higher prices ahead. Meanwhile, World Steel Dynamics reported that large-volume buyers were “ready” to enter the market, just as mill capacity faced temporary cuts.

Unfortunately for mills, those warnings translated to a modest and temporary price increase, which began to unravel by the second half of April.

Steel Prices Flatten Amid Bearish Signals

Now, roughly four months later, the market faces similar warnings of a turnaround. For example, both Nucor and Cleveland Cliffs raised their consumer spot prices at the start of August. Cliffs held at the top of the market, with prices rising from $670/st at the end of July to $700/st five days later. Meanwhile, Nucor saw two consecutive increases, including a raise to $650 on July 22 to $675/st on July 29 and to $690/st on August 5.Z

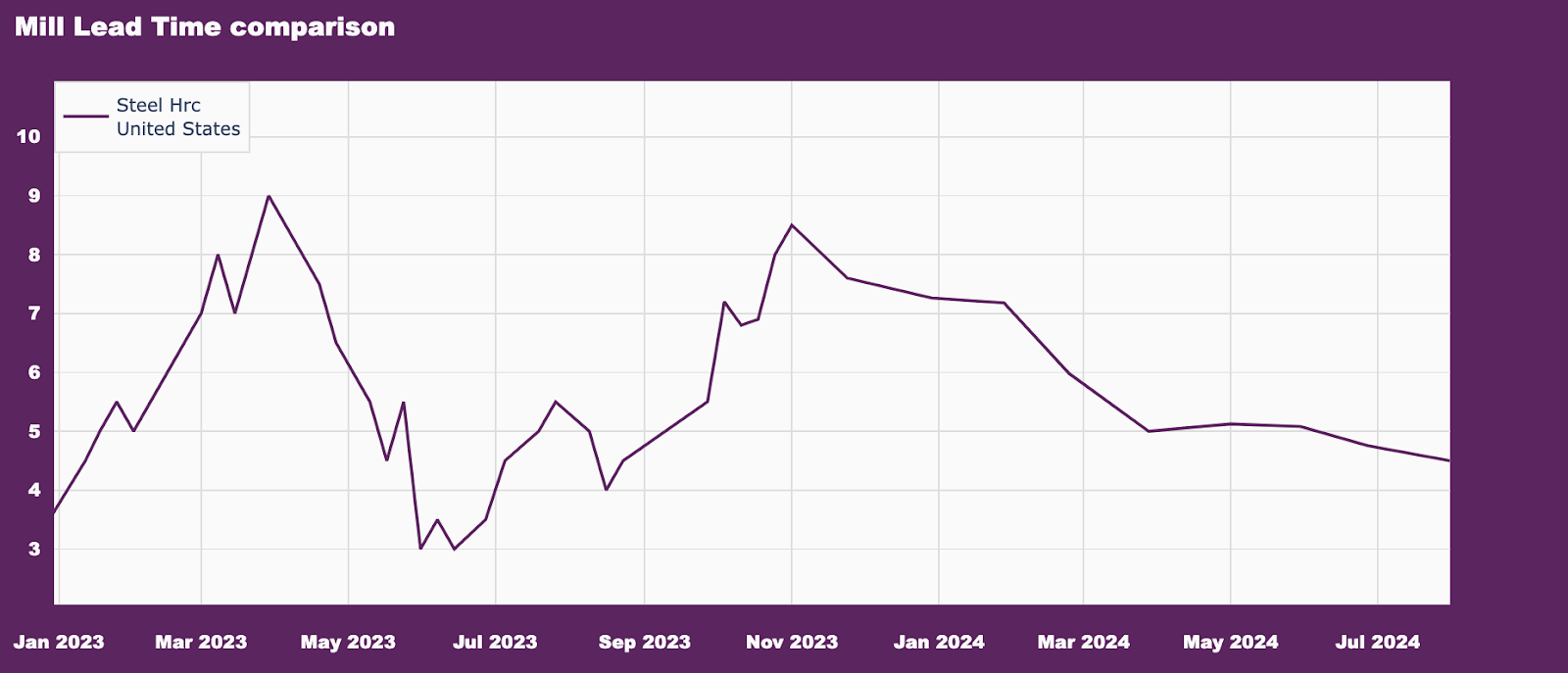

While the warnings echo those of April, market conditions have shifted and, to some extent, worsened. Mill lead times temporarily lengthened, albiet modestly, beginning in March, which would suggest tightening supply conditions. However, the opposite appeared true by the close of July, as mill lead times continued to shorten and slip below their historical averages across the flat rolled steel category.

Working in the mills’ favor is the fact that destocking efforts and limited buying activity saw distributor inventory levels reportedly dip beneath their historical average over recent months. This offers service centers less cushion to hold off purchasing activity if mills hold firm on pricing.

That said, demand conditions have yet to turn around amid the cumulative effect of rate hikes, which will offer little incentive to place large volume orders. Meanwhile, the ISM Manufacturing PMI retreated further into contraction, moving from 48.5 in June to 46.8 in July. This continues to force an increasing number of manufacturers to resort to layoffs.

Seasonality Offers Little Insight to Steel Prices

Looking back, historical trends offer little definitive insight into how prices will fare throughout Q3. Considering the price action witnessed between 2012-2023, average steel prices do not show a consistent trend up or down from the previous quarter, nor do they show a meaningful year-over-year correlation.

ADVERTISEMENT

While seasonality impacts buying patterns, a number of factors still determine pricing. Most important of all is capacity discipline on the part of mills, which helps ensure supply remains balanced with demand. While much could change throughout the next month, the shorter mill lead times witnessed last month suggest mills will seemingly require more meaningful cuts to supply, especially as demand conditions continue to disappoint.

By Nichole Bastin

More Top Reads From Oilprice.com

- CNOOC Adds Massive Gas Reserves in South China Sea Discovery

- After Campaigning on Free Natural Gas, Erdogan Hikes Prices by 38%

Lower LNG Prices Drag Cheniere’s Q2 Profit Down by 36%