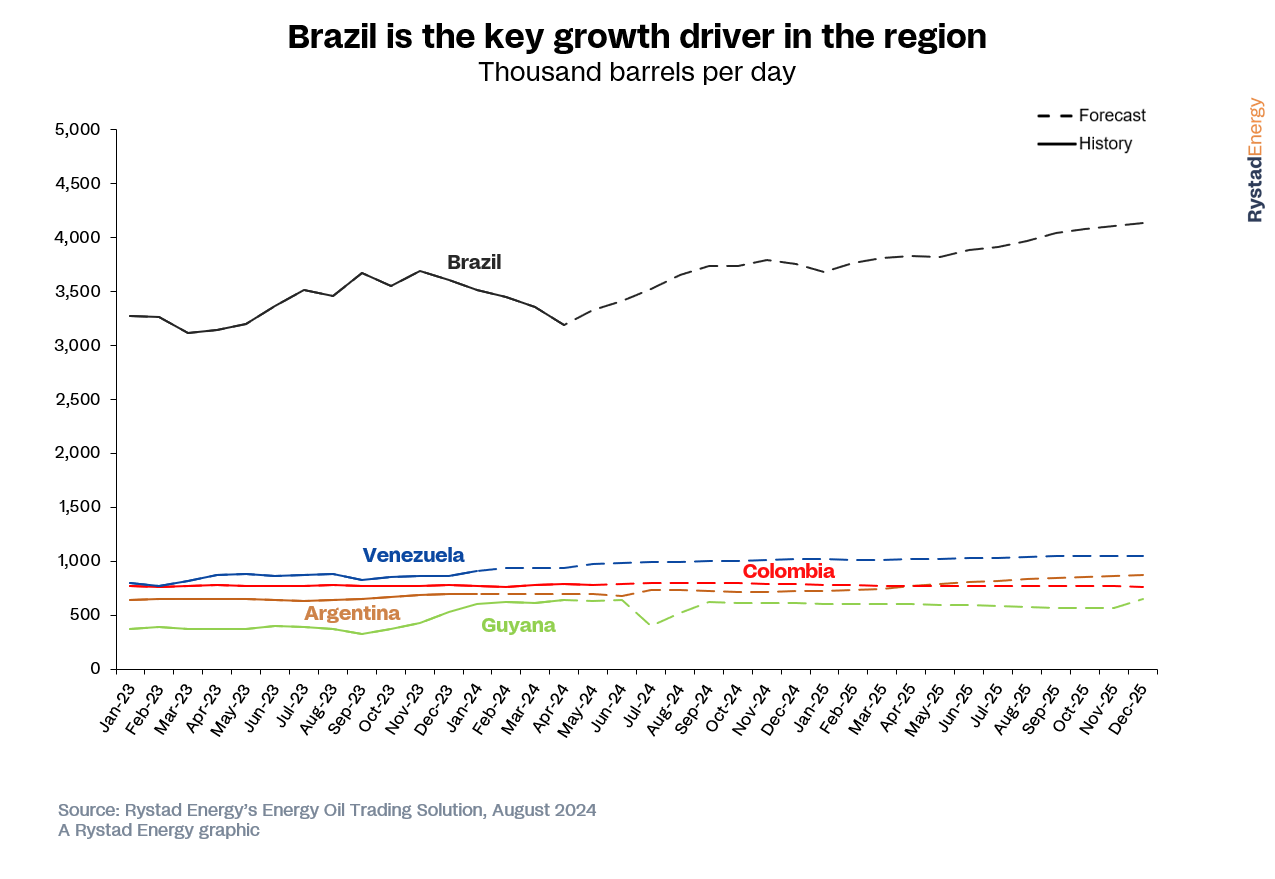

South America is a key source for growth in the world’s crude oil supply as production in other regions is stagnating. Brazil, Guyana and Argentina are among the fastest-growing countries in terms of crude supply growth, and Venezuela has also seen a good recovery in recent months. The latest data shows Brazil’s crude and condensate output climbed 7% from April to June, halting a five-month declining trend. Guyana’s rapid output growth slowed in the third quarter as key assets underwent maintenance, while shale oil production in Argentina will continue to rise throughout this year and next as the Vaca Muerta shale play grows exponentially.

Elsewhere in South America, Colombia is expected to see a strong third quarter this year with average production of 797,000 barrels per day, rising by 12,000 bpd from the preceding quarter. The country’s output is projected to decline starting in the fourth quarter and through 2025 as production from mature declines.

Brazil

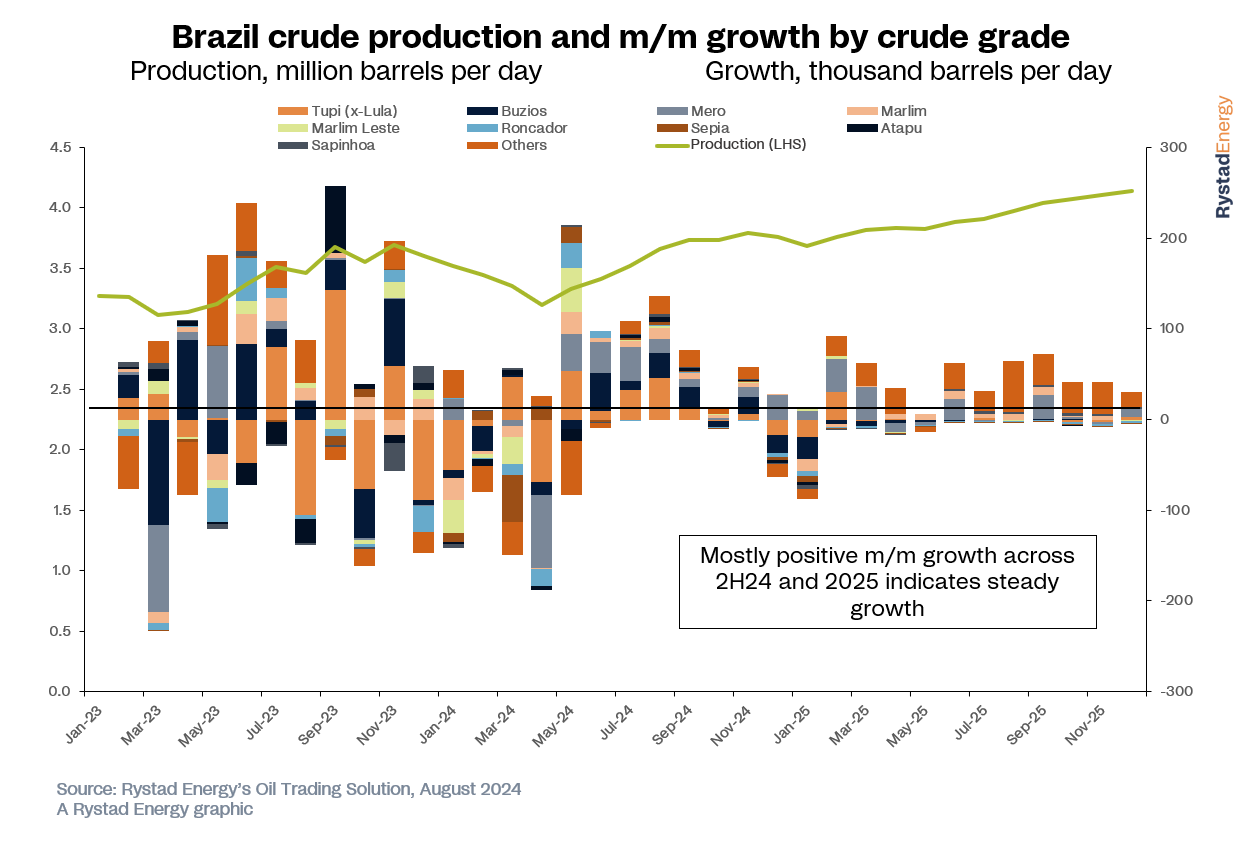

After a steady decline in the first quarter this year due to a wave of maintenance and other outages across Petrobras-operated assets, Brazilian crude output has been recovering since the low in April. May recorded an output level of almost 3.33 million bpd of crude and condensate, a 132,000-bpd month-on-month increase. The top-line figure reported for June is 3.41 million bpd, adding another 87,000 bpd m/m. Rystad Energy expects the country’s production to rise further by 107,000 bpd m/m in July to 3.52 million bpd and keep rising to bring Brazil’s exit rate for 2024 to 3.76 million bpd.

The major driver of this growth is the ramp-up in production of the country’s three key crude grades – Tupi, Buzios and Mero. These three grades combined are expected to grow by almost 240,000 bpd in the third quarter. Marlim and Marlim Leste grades also rose significantly in May at around 25,000 bpd and 48,000 bpd, respectively. The increase in production comes as assets ramp up after the previously mentioned outages.

Next year is anticipated to bring strong growth in Brazil of almost 400,000 bpd to more than 3.9 million bpd on average for 2025, led by new startups at the Mero and Buzios fields along with the new Bacalhau project. Mero 3, Buzios 7, and Bacalhau Phase 1 are the largest assets scheduled to come online by the end of 2025 and are anticipated to add up to 460,000 bpd combined by the end of 2025.

The Mero 3 startup date has been pushed to November this year as the FPSO Marechal Duque de Caxias only arrived in May. Similarly, the FPSO Maria Quiteria on the Jubarte field is scheduled to start up in December 2024 and ramp up to over 90,000 bpd by the end of next year.

Brazilian crude exports remained flat m/m at around 1.5 million bpd in July. In fact, the level has stayed almost the same since May this year. China was the largest consumer of Brazilian barrels in July with almost 690,000 bpd, corresponding to almost 45% of Brazil’s total crude exports. Brazilian exports have been at the lower end since December 2023 due to falling production levels, however we can anticipate rising exports in the coming months as crude production recovers.

Venezuela

Venezuela is anticipated to produce 932,000 bpd of crude oil this month, adding 4,000 bpd from July and continuing the trend of steady m/m growth as reported by OPEC+ in its Monthly Oil Market Report. The country’s crude output has increased gradually since the first easing of sanctions in 4Q23 and has continued to grow even after the reimposition in April 2024.

The current iteration of our data maintains a positive outlook for Venezuela with a healthy growth rate projected for this year and next with, adding 126,000 bpd in 2024 and 62,000 bpd in 2025. Country-level output for Venezuela is now projected to average 940,000 bpd in 2H24, though this forecast is subject to change following the recent result of the controversial elections held in the country. The upcoming US election is also likely to impact the future of Venezuela’s crude outlook.

In the latest data iteration, Venezuela’s crude production outlook has been revised down marginally, by around 6,000 bpd in 2H24 and by 11,000 bpd across 2025. The entirety of the revisions are made to the output of the Urdaneta Oeste (West) asset as the half-yearly report by operator Maurel & Prom showed lower-than-projected actualized production of 13,500 bpd, compared to its earlier target of 25,000 bpd in gross field-level output by the end of the year.

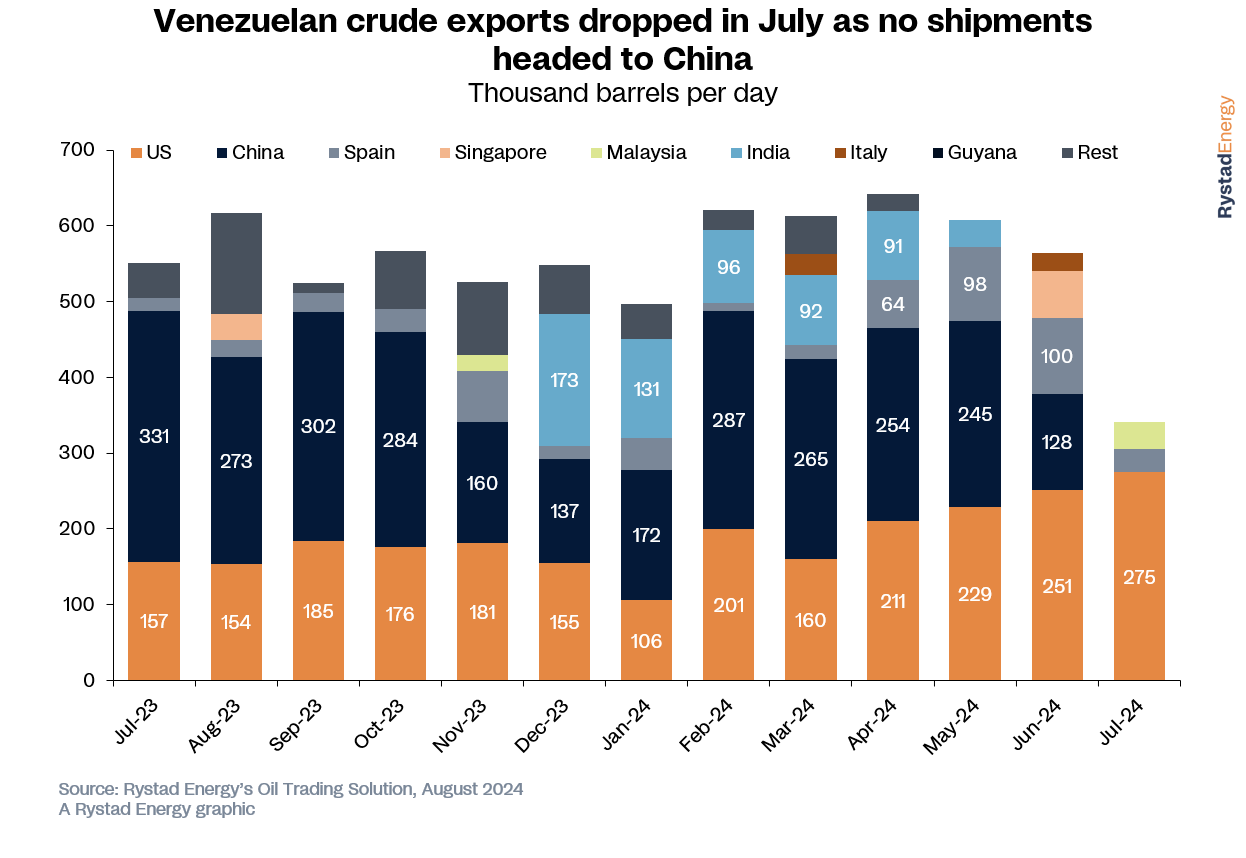

Venezuela’s exports declined by over 230,000 bpd in July as exports to China diminished. Outages at certain blending and processing units that process output from the Orinoco belt led to unavailability of diluted crude and increased delays in loading cargoes and exports in July. The elections held in the country during the period also affected exports negatively as July exports averaged just 340,000 bpd. The US, China and Spain were the largest consumers of Venezuelan barrels in 2Q24.

Guyana

Guyana’s crude and condensate production for August is projected to average around 520,000 bpd. This is a significant 120,000 bpd m/m jump from July’s average of 400,000 bpd, but well below the country’s first-half average of 626,000 bpd.

Under the Gas-to-Energy (GTE) project, ExxonMobil paused production at the Liza Unity in July to install and tie back a 12-inch gas pipeline to the FPSO to transport gas onshore to the Wales development site, West Bank Demerara, where it is to be used as a power-generation source. Guyana’s government plans to use around 50 million cubic feet per day of gas to generate 300 megawatts of electricity. The Liza Destiny was shut in August for the same reason.

Crude output from the Liza field is expected to recover promptly and return to normal by September. We expect Guyana to produce over 610,000 bpd in the fourth quarter this year, bringing 2024’s average to 593,000 bpd. Average crude production across 2025 is expected to be relatively flat, though we expect to see a jump in output levels in 4Q25 as the FPSO One Guyana comes online at the Yellowtail field.

Argentina

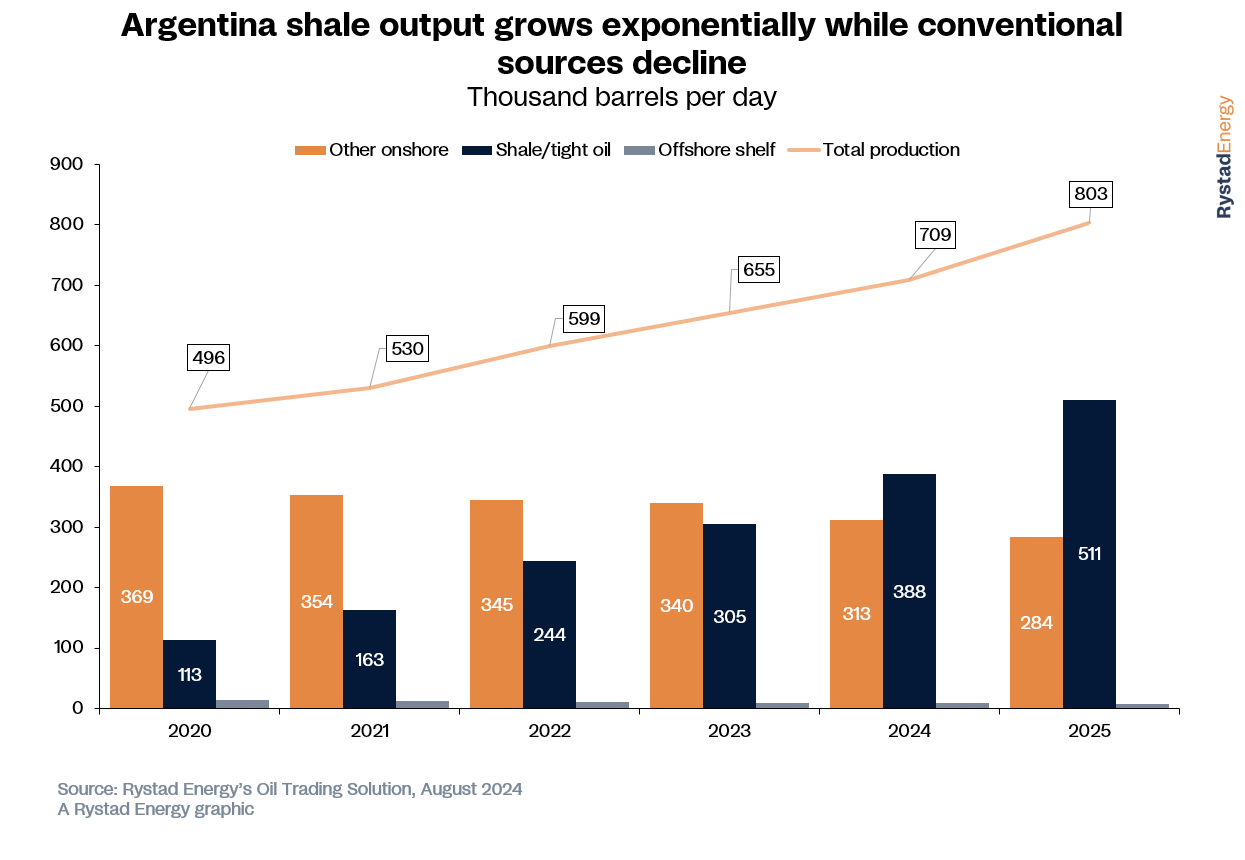

Argentina is a key supply growth driver in Latin America. The nation’s production grew by over 7% y/y in 2Q24 to 691,000 bpd on average. This year and next are projected to be strong years for Argentina’s production, with anticipated growth of 8% in 2024 and 13% next year. Current estimates show the country is expected to breach the 800,000-bpd production mark in the second half of 2025, overtaking Colombia which is projected to decline steadily across next year due to its mature assets.

ADVERTISEMENT

Shale production from is driving Argentina’s output growth, while other onshore sources steadily decline. Crude and condensate output is expected to average around 733,000 bpd this month, 56% of which comes from shale. This volume indicates an over 14% y/y increase in output.

The Vaca Muerta shale play has had an impressive growth rate since 2023 and accounts for over half of total production from the country. The growth rate is enhanced by a steady output increase for several small assets under the project and sustained production levels from the largest assets such as Loma Campana and La Amarga Chica, which average around 85,000 bpd and 65,000 bpd, respectively.

More Top Reads From Oilprice.com

- UAE’s State Oil Giant ADNOC Issues First-Ever Bond

- Controversy Surrounds Kazakhstan's Nuclear Referendum

- India Proposes Anti-Dumping Duties on Chinese Aluminum Foil